Foreign Source Income Taxable In Malaysia / If you are a foreigner that has stayed and worked in malaysia for more than 182 days during the calendar year, you have a resident status and you will fall under the normal malaysian tax laws that are also applicable to the native population, check out all information on this taxing system in this article.

Foreign Source Income Taxable In Malaysia / If you are a foreigner that has stayed and worked in malaysia for more than 182 days during the calendar year, you have a resident status and you will fall under the normal malaysian tax laws that are also applicable to the native population, check out all information on this taxing system in this article.. As a starting point you are liable. 1.4 foreign investment 1.5 tax incentives 1.6 exchange controls 2.0 setting up a business 2.1 principal forms of business entity 2.2 regulation of business 2.3 accounting, filing and auditing requirements 3.0 business taxation 3.1 overview 3.2 residence 3.3 taxable income and rates 3.4 capital gains taxation 3.5 double taxation relief When adam filed his income tax returns in malaysia for the year of assessment 2010 on 30.4.2011, he did not make a claim for any bilateral credit as he had lost all the relevant information and documentation on the tax paid in the uk. Malaysia has adopted a territory basis for taxation where only income derived from malaysia is taxable in malaysia except for the business of banking, insurance and sea or air transportation. If income (not capital gains) derived from outside malaysia is remitted to malaysia, that is, sent back to or received in malaysia, it is conceptually subject to tax in malaysia, but malaysia has introduced law (schedule 6, paragraph 28) to specifically exempt such income.

If income (not capital gains) derived from outside malaysia is remitted to malaysia, that is, sent back to or received in malaysia, it is conceptually subject to tax in malaysia, but malaysia has introduced law (schedule 6, paragraph 28) to specifically exempt such income. 1.4 foreign investment 1.5 tax incentives 1.6 exchange controls 2.0 setting up a business 2.1 principal forms of business entity 2.2 regulation of business 2.3 accounting, filing and auditing requirements 3.0 business taxation 3.1 overview 3.2 residence 3.3 taxable income and rates 3.4 capital gains taxation 3.5 double taxation relief If the fees are derived from a country other than malaysia, they are not taxed. Companies operating in malaysia (resident status) are under the following corporate tax rates: Think of it as investing rm6,000 for your future self with the bonus of getting a sweet tax exemption.

Why Investors Should Consider Taxable Municipal Bonds ... from www.advisorperspectives.com Starting the year of assessment 2016, resident sdn bhd, i.e. However, the tax code has a provision which exempts you from such tax. The dividend tax, which is income tax levied on the dividend by the foreign country of source; Here is an overview of income tax and taxable benefits in malaysia, as a guide to get you started, and suggestions on getting the help you need to stay in compliance. Fees are deemed to be derived from malaysia if the company is resident in malaysia for the year of assessment. If you are a foreigner that has stayed and worked in malaysia for more than 182 days during the calendar year, you have a resident status and you will fall under the normal malaysian tax laws that are also applicable to the native population, check out all information on this taxing system in this article. Knowhow von über 200 aktiven bergsportlern. For the most part, foreigners working in malaysia are divided into two categories:

Section 3 of the ita extends its territorial scope to include foreign source income received in malaysia from outside malaysia.

If you repatriate that income back into malaysia, you will theoretically be taxed. Malaysia adopts a territorial approach to income tax. With effect from ya 2004, foreign source income derived from sources outside malaysia and received in malaysia by any person is not subject to malaysian income tax section 12 of the income tax act, 1967 is about the determining the source of income or derivation of income Section 3 of the ita extends its territorial scope to include foreign source income received in malaysia from outside malaysia. Here is an overview of income tax and taxable benefits in malaysia, as a guide to get you started, and suggestions on getting the help you need to stay in compliance. Malaysia has a territorial income tax system, meaning that income tax in malaysia is only imposed on income accruing in or derived from malaysia. When adam filed his income tax returns in malaysia for the year of assessment 2010 on 30.4.2011, he did not make a claim for any bilateral credit as he had lost all the relevant information and documentation on the tax paid in the uk. If the fees are derived from a country other than malaysia, they are not taxed. And the underlying tax, which is income tax paid or payable by the dividend paying company on the income out of which the dividend is paid. 1.4 foreign investment 1.5 tax incentives 1.6 exchange controls 2.0 setting up a business 2.1 principal forms of business entity 2.2 regulation of business 2.3 accounting, filing and auditing requirements 3.0 business taxation 3.1 overview 3.2 residence 3.3 taxable income and rates 3.4 capital gains taxation 3.5 double taxation relief Über 500 marken mit mehr als 40.000 artikel. An employee is taxed on employment income earned for work performed in malaysia regardless of where payment is made. Foreign source income, however, when received in malaysia by a resident company (other than a company carrying on the business of banking, insurance, air and sea transport) is exempt from tax.

But i want to emphasize that there is no free lunch, because that income would have been taxed at that foreign source. Starting the year of assessment 2016, resident sdn bhd, i.e. Paragraph 28 schedule 6 income tax act 1967 provides that the income derived from sources outside malaysia is exempt from tax. An employee is taxed on employment income earned for work performed in malaysia regardless of where payment is made. If the fees are derived from a country other than malaysia, they are not taxed.

Calculate taxable income of company in australia example from image.slidesharecdn.com Malaysia has adopted a territory basis for taxation where only income derived from malaysia is taxable in malaysia except for the business of banking, insurance and sea or air transportation. The salary earned from working abroad would not be taxable unless the income received is in respect of duties incidental to the exercise of employment in malaysia. In that case, you'll only pay tax in malaysia on income that you earn there. Foreign source income, however, when received in malaysia by a resident company (other than a company carrying on the business of banking, insurance, air and sea transport) is exempt from tax. Here is an overview of income tax and taxable benefits in malaysia, as a guide to get you started, and suggestions on getting the help you need to stay in compliance. Taxable on the same income in malaysia and in the uk. Subject to tax condition for substantive business activities Taxation of investment income and capital gains are investment income and capital gains taxed in malaysia?

However, income of a resident company from the business of air/sea transport, banking, or insurance is assessable on a worldwide basis.

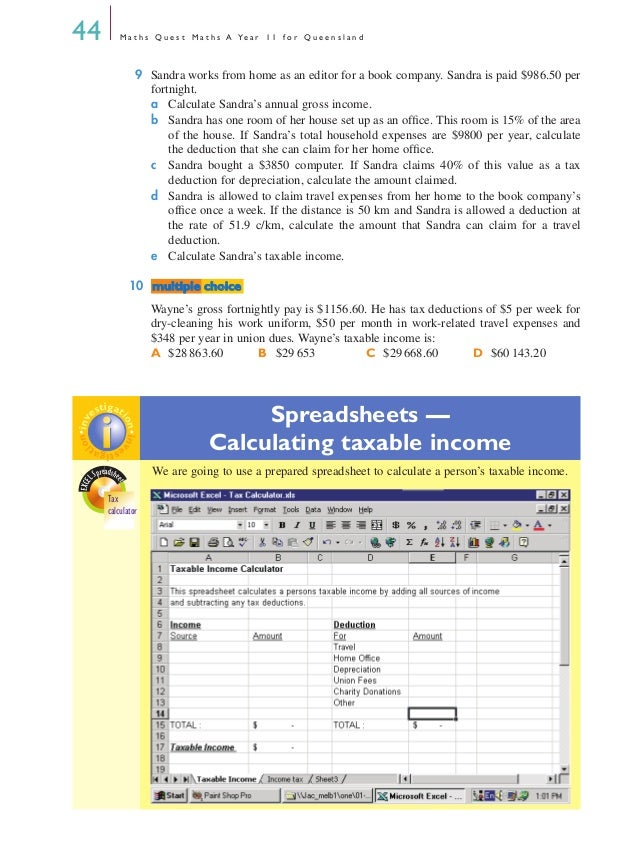

If you repatriate that income back into malaysia, you will theoretically be taxed. Malaysia has a territorial income tax system, meaning that income tax in malaysia is only imposed on income accruing in or derived from malaysia. For the most part, foreigners working in malaysia are divided into two categories: Malaysia has adopted a territory basis for taxation where only income derived from malaysia is taxable in malaysia except for the business of banking, insurance and sea or air transportation. In other words, being a mm2h resident of malaysia means all your foreign sourced income, including pension, interest, and dividend income, as well as foreign earned income, is exempt from malaysian taxes. Taxation of investment income and capital gains are investment income and capital gains taxed in malaysia? Companies operating in malaysia (resident status) are under the following corporate tax rates: Here is an overview of income tax and taxable benefits in malaysia, as a guide to get you started, and suggestions on getting the help you need to stay in compliance. Paragraph 28 schedule 6 income tax act 1967 provides that the income derived from sources outside malaysia is exempt from tax. When adam filed his income tax returns in malaysia for the year of assessment 2010 on 30.4.2011, he did not make a claim for any bilateral credit as he had lost all the relevant information and documentation on the tax paid in the uk. But again, the devil is in the detail. As a starting point you are liable. The dividend tax, which is income tax levied on the dividend by the foreign country of source;

Subject to tax condition for substantive business activities With effect from ya 2004, foreign source income derived from sources outside malaysia and received in malaysia by any person is not subject to malaysian income tax section 12 of the income tax act, 1967 is about the determining the source of income or derivation of income The mita taxes income accrued or derived from malaysia or received in malaysia from outside malaysia. Foreign source income, however, when received in malaysia by a resident company (other than a company carrying on the business of banking, insurance, air and sea transport) is exempt from tax. In other words, being a mm2h resident of malaysia means all your foreign sourced income, including pension, interest, and dividend income, as well as foreign earned income, is exempt from malaysian taxes.

Understanding Foreign-Sourced Income - Malaysian Income Tax from www.malaysiataxation.com Foreign source income, however, when received in malaysia by a resident company (other than a company carrying on the business of banking, insurance, air and sea transport) is exempt from tax. With effect from ya 2004, foreign source income derived from sources outside malaysia and received in malaysia by any person is not subject to malaysian income tax section 12 of the income tax act, 1967 is about the determining the source of income or derivation of income Knowhow von über 200 aktiven bergsportlern. 1.4 foreign investment 1.5 tax incentives 1.6 exchange controls 2.0 setting up a business 2.1 principal forms of business entity 2.2 regulation of business 2.3 accounting, filing and auditing requirements 3.0 business taxation 3.1 overview 3.2 residence 3.3 taxable income and rates 3.4 capital gains taxation 3.5 double taxation relief When adam filed his income tax returns in malaysia for the year of assessment 2010 on 30.4.2011, he did not make a claim for any bilateral credit as he had lost all the relevant information and documentation on the tax paid in the uk. But i want to emphasize that there is no free lunch, because that income would have been taxed at that foreign source. Malaysia has a territorial income tax system, meaning that income tax in malaysia is only imposed on income accruing in or derived from malaysia. Veerinderjeet noted that malaysia has a wonderful territorial system that only imposes tax on income derived from the country, as foreign income derived outside malaysia is not taxable.

But again, the devil is in the detail.

Starting the year of assessment 2016, resident sdn bhd, i.e. However, the tax code has a provision which exempts you from such tax. That means you'll have to pay tax on your worldwide income to malaysia. Paragraph 28 schedule 6 income tax act 1967 provides that the income derived from sources outside malaysia is exempt from tax. For the most part, foreigners working in malaysia are divided into two categories: References for income tax act, 1967 section 3 income tax act, 1967 (ita) says that income shall be charged for the income of any person accruing in or derived from malaysia or received in or from malaysia. According to malaysian tax code, you will not be subjected to malaysian income tax for income you derived overseas. Malaysia has adopted a territory basis for taxation where only income derived from malaysia is taxable in malaysia except for the business of banking, insurance and sea or air transportation. 1.4 foreign investment 1.5 tax incentives 1.6 exchange controls 2.0 setting up a business 2.1 principal forms of business entity 2.2 regulation of business 2.3 accounting, filing and auditing requirements 3.0 business taxation 3.1 overview 3.2 residence 3.3 taxable income and rates 3.4 capital gains taxation 3.5 double taxation relief If you are a foreigner that has stayed and worked in malaysia for more than 182 days during the calendar year, you have a resident status and you will fall under the normal malaysian tax laws that are also applicable to the native population, check out all information on this taxing system in this article. Veerinderjeet noted that malaysia has a wonderful territorial system that only imposes tax on income derived from the country, as foreign income derived outside malaysia is not taxable. Taxation for foreign owned sdn bhd. The salary earned from working abroad would not be taxable unless the income received is in respect of duties incidental to the exercise of employment in malaysia.

Related : Foreign Source Income Taxable In Malaysia / If you are a foreigner that has stayed and worked in malaysia for more than 182 days during the calendar year, you have a resident status and you will fall under the normal malaysian tax laws that are also applicable to the native population, check out all information on this taxing system in this article..